Crypto Tax Enforcement and Penalties in India: What You Need to Know in 2026

Jan, 14 2026

Jan, 14 2026

India’s crypto tax rules aren’t just complicated-they’re designed to make trading as unattractive as possible. Since April 2022, the government has treated cryptocurrency gains like lottery winnings: 30% tax, no loss offsets, and no deductions. But what happens if you don’t pay? And how does the government even find out you traded Bitcoin or Ethereum? The answers aren’t obvious, but the consequences are real.

How Crypto Gains Are Taxed in India

If you bought Bitcoin for ₹5 lakh and sold it for ₹8 lakh, you made a ₹3 lakh profit. Under Section 115BBH of the Income Tax Act, you owe 30% of that-₹90,000-no matter how long you held it. No lower rates for long-term holds. No way to reduce your tax bill by claiming losses from other trades. Even if you lost ₹5 lakh on Solana and made ₹1 lakh on Cardano, you still pay 30% on the ₹1 lakh gain. Losses? They disappear. You can’t carry them forward. You can’t use them to offset other income.

This isn’t just strict-it’s unique. Most countries allow you to offset crypto losses against gains. India doesn’t. The government’s message is clear: if you’re gambling on crypto, you’re on your own.

The 1% TDS That’s Tracking Every Trade

Every time you sell crypto on an Indian exchange, the buyer (or the exchange acting as buyer) must deduct 1% of the sale value as Tax Deducted at Source (TDS). That’s under Section 194S. If you sell ₹10 lakh worth of Ethereum, ₹10,000 gets taken out before you even see the money.

This isn’t optional. Exchanges like WazirX, CoinSwitch, and ZebPay are legally required to do this. They report every transaction to the Income Tax Department. The government gets a real-time log of who sold what, when, and for how much. If you trade on an Indian platform, they’re already sending your data to the tax authorities.

But here’s the loophole: peer-to-peer (P2P) trades. If you buy Bitcoin directly from someone using UPI or bank transfer, and no exchange is involved, TDS doesn’t apply. But that doesn’t mean you’re safe. The government can still track bank transfers linked to crypto purchases through financial intelligence units. And if you report the income, they’ll cross-check your bank statements with your tax return.

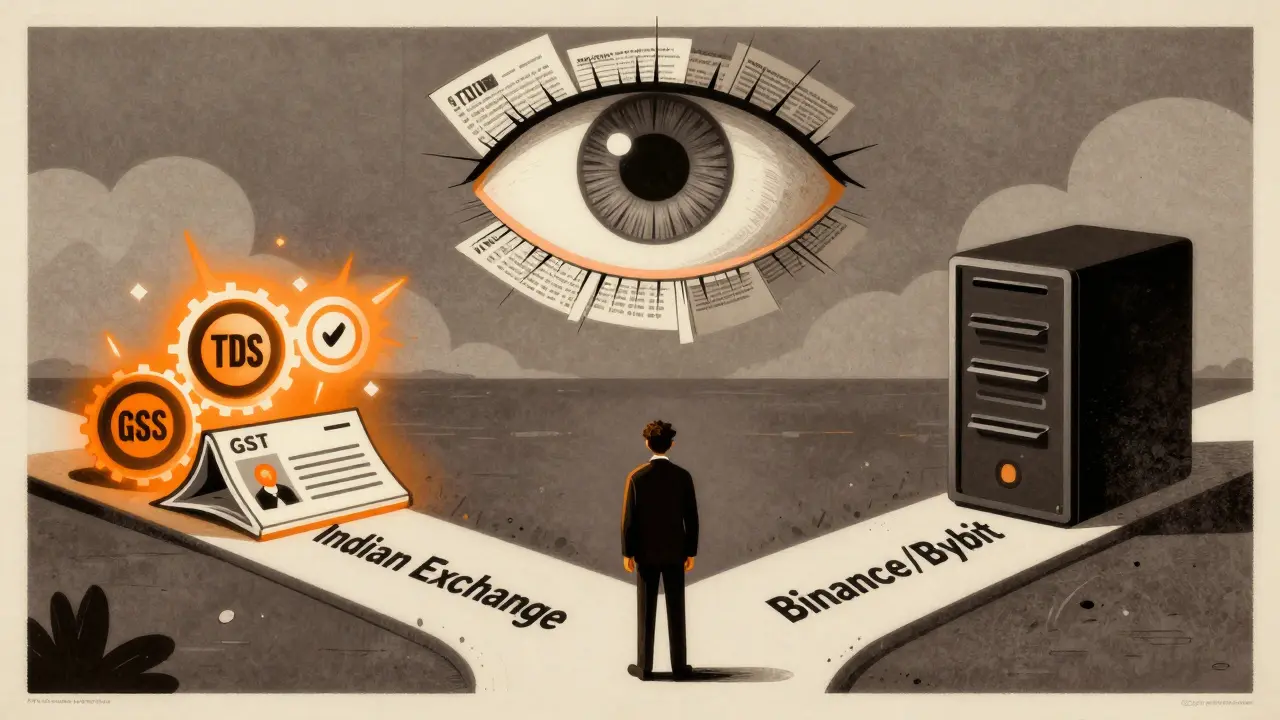

GST on Crypto Services-Now It’s Everywhere

Starting July 7, 2025, anything you pay to a crypto platform in India is taxed at 18% GST. That includes:

- Trading fees

- Withdrawal charges

- Deposit fees

- Staking rewards management

- Wallet services

- KYC verification fees

Even if you’re just holding crypto in a wallet provided by an Indian exchange, you’re paying GST. And platforms? They must register for GST regardless of turnover. That’s unusual. Most small businesses don’t need to register unless they hit ₹20 lakh in sales. Crypto platforms? They have to register even if they make ₹50,000 a year.

This isn’t just about revenue. It’s about control. By forcing platforms to issue GST invoices and keep digital records, the government creates a paper trail. Every transaction is traceable. Every fee, every withdrawal, every staking payout-it’s all logged.

How You Report Crypto Income

If you made money from crypto in FY 2024-25, you must file either ITR-2 or ITR-3. Both forms now include a dedicated section called ‘Schedule VDA’ (Virtual Digital Assets). You need to list:

- Each crypto asset you traded

- Cost of acquisition

- Sale price

- Net gain or loss

- TDS deducted

Even if your net gain is zero because you lost money overall, you still have to report every single trade. No exceptions. The system is built to catch underreporting. If you report ₹2 lakh in gains but your exchange shows ₹8 lakh in sales, the IT department will notice.

And if you’re mining crypto or receiving airdrops? Those are taxed too. The value is calculated based on the fair market price on the day you received it, using Rule 11UA of the Income Tax Rules. If you got 0.5 ETH as an airdrop when it was worth ₹1.2 lakh, that’s ₹1.2 lakh of taxable income-even if you never sold it.

What Happens If You Don’t Pay?

There’s no official list of crypto-specific penalties. That’s because India doesn’t have a separate law for crypto tax evasion. Instead, it uses existing income tax rules.

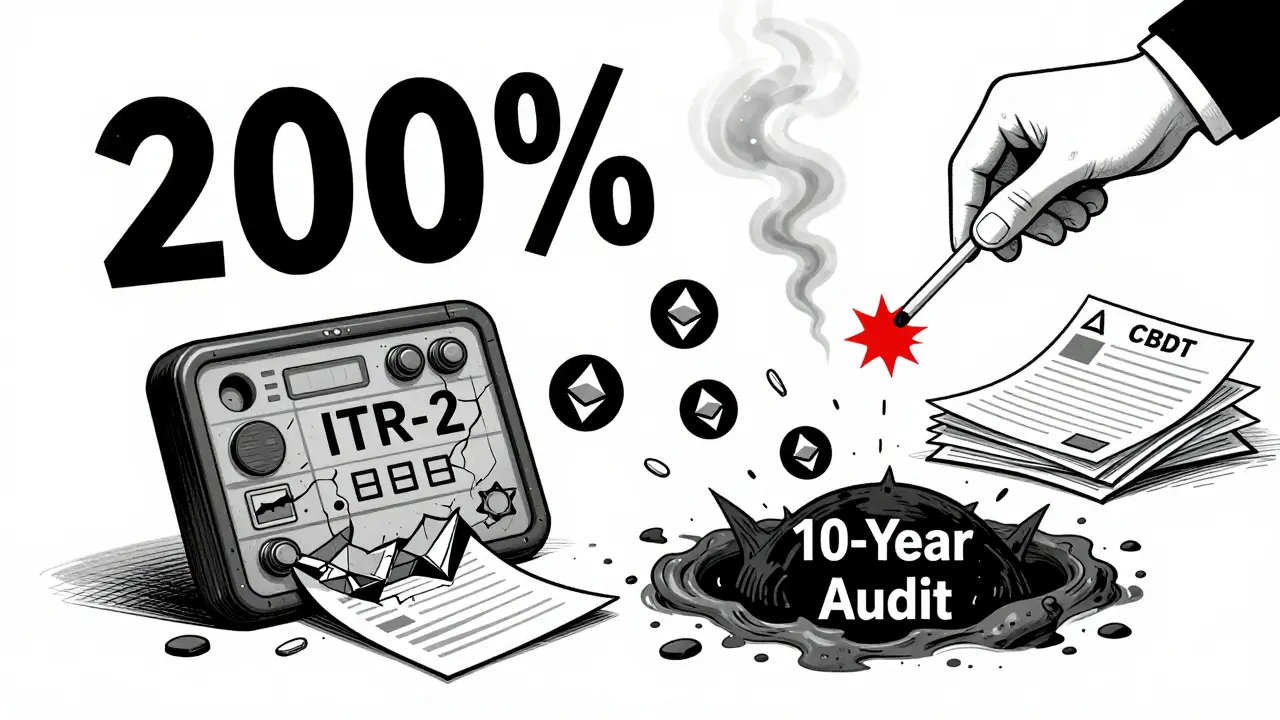

Under Section 271(1)(c), if you underreport income, you can be fined up to 200% of the tax evaded. So if you owed ₹1 lakh in crypto taxes and didn’t pay, you could face a ₹2 lakh penalty. Add interest under Section 234A, 234B, and 234C-up to 1% per month on unpaid tax. That adds up fast.

Worse, if the tax department believes you’re hiding income deliberately, they can reopen your tax return for up to 10 years. That means if you traded crypto in 2022 and didn’t report it, they can come after you in 2032.

And they’re getting better at finding you. The Income Tax Department has direct access to data from exchanges. They’ve also partnered with banks to flag suspicious crypto-linked transfers. If your bank account suddenly receives ₹15 lakh from a crypto wallet, and you didn’t report it, you’re on their radar.

Why Enforcement Is Still a Challenge

Despite all this, enforcement is patchy. Why? Because crypto is decentralized. You can trade on offshore platforms like Binance or Bybit without ever touching an Indian exchange. No TDS. No GST. No Indian platform reporting your trade.

And that’s where the real gap is. The government can track trades on Indian platforms-but not those done overseas. Yet, if you bring those profits back to India-say, by cashing out to your Indian bank account-they can still trace it. Large, unexplained deposits trigger automated alerts.

Also, mining and staking are nearly impossible to monitor. If you mine Bitcoin from your home computer, there’s no third party to report it. The government has no way of knowing unless you tell them. But if you later sell that Bitcoin on an Indian exchange, the tax trail starts there.

That’s why the Central Board of Direct Taxes (CBDT) started asking tough questions in August 2025: Is the 1% TDS too heavy? Is the 30% rate killing liquidity? Are offshore exchanges giving users an unfair advantage?

The answers to those questions might change the rules soon.

What’s Next for Crypto Tax in India?

Right now, the system feels more like a deterrent than a revenue tool. The 30% rate is among the highest in the world. The TDS rule forces compliance at every step. The GST rules extend the net to every service around crypto.

But the results? Trading volumes on Indian exchanges have dropped by nearly 60% since 2022. Many startups have moved operations to Dubai, Singapore, or Portugal. Retail investors are staying away. The government isn’t collecting as much as it hoped.

The CBDT’s review suggests they know this. A new law could be coming-maybe one that treats crypto like securities, with capital gains rules and loss offsets. Or maybe they’ll double down and add even stricter penalties.

For now, the safest move is simple: report everything. Even if you think you won’t get caught. The risk of a 200% penalty, 10-year audit, and legal trouble isn’t worth saving a few thousand rupees in taxes.

What You Should Do Today

- Collect all your trade history from every exchange you used in 2024-25.

- Calculate your gains and losses separately for each asset.

- Check your bank statements for any crypto-related deposits or withdrawals.

- File ITR-2 or ITR-3 with Schedule VDA filled out completely.

- If you used offshore platforms, keep records of purchase and sale prices in case the tax department asks.

- Don’t wait until the last minute. The system is watching.

India’s crypto tax system isn’t designed to be fair. It’s designed to discourage. But if you play by the rules, you won’t get punished. If you ignore them? You’re playing with fire-and the government has the matches.

Ashlea Zirk

January 15, 2026 AT 13:35The 30% tax on crypto gains without loss offset is economically irrational. It treats speculative assets like gambling winnings, ignoring the fundamental difference between risk-taking investment and pure chance. The government's approach may deter retail participation, but it also stifles innovation in a sector that could otherwise contribute meaningfully to fintech infrastructure. Compliance burden outweighs revenue gain when legitimate traders flee to jurisdictions with balanced frameworks.

Moreover, the 1% TDS on every transaction creates friction that disincentivizes micro-trading and liquidity provision. While it improves traceability, it also penalizes small participants disproportionately. A tiered system based on transaction volume or holding period would be more equitable and efficient.

Additionally, GST on wallet services and KYC fees is a regulatory overreach. These are operational costs, not consumption goods. Taxing them is akin to taxing the cost of maintaining a bank account. It creates a cascading tax effect that ultimately gets passed on to users, reducing accessibility.

The real issue isn't tax evasion-it's design failure. A system that assumes bad faith from the outset will always breed distrust. Instead of surveillance-heavy enforcement, India could lead by building a transparent, rules-based framework that rewards compliance through clarity and fairness.

Other nations are moving toward classification as capital assets. India risks becoming an outlier, not a leader. The drop in trading volume isn't a victory-it's a warning sign.

Shaun Beckford

January 15, 2026 AT 17:00This whole system is a glorified tax trap dressed up as policy. 30% on gains? No loss carryforwards? You’re basically saying ‘fuck you’ to anyone who didn’t buy Bitcoin at $300 and cashed out at $60k. And now they slap 18% GST on every damn withdrawal fee like we’re buying overpriced lattes?

Meanwhile, some dude in Goa is mining ETH in his garage with a rigged GPU rig and zero paperwork. But if you use WazirX? Boom-TDS gets auto-deducted and your data gets fed straight to the IT dept like a fucking data sausage. Hypocritical as hell.

And don’t even get me started on the 10-year audit loophole. That’s not tax enforcement-that’s legal terrorism. You think they’re gonna catch me? Nah. I’m just gonna hold until the next regime changes and then cash out through a friend’s NRE account. Game on, Uncle Sam-I mean, Uncle Modi.

PS: If you report your airdrops, you’re a sucker. They’ll never find you if you don’t move it to an Indian bank. Just sayin’.

Chris Evans

January 16, 2026 AT 06:57The architecture of this tax regime reflects a deeper ontological crisis in state-crypto relations. The state, as a centralized epistemic authority, cannot reconcile with decentralized, pseudonymous value networks. Hence, it responds not with adaptation, but with overcompensation-30% taxation as a performative act of sovereignty, TDS as a panopticon of transactional visibility, GST on infrastructure fees as a symbolic assertion of regulatory hegemony.

What we’re witnessing is not fiscal policy, but epistemic violence. The state attempts to domesticate the wild, non-sovereign ontology of crypto by forcing it into the rigid taxonomies of fiat logic: capital gains, income streams, taxable events. But crypto operates on a different temporal and ontological plane-its value is emergent, not derived.

The 1% TDS isn’t a revenue tool-it’s a psychological weapon. It conditions users to perceive every trade as a potential audit trigger. This transforms financial autonomy into performative compliance. The result? Not higher revenues, but a quiet exodus of capital and talent toward jurisdictions that treat crypto as a technological paradigm, not a tax evasion vector.

And yet… the government’s fear is understandable. Decentralization threatens the monopoly on monetary narrative. The real question isn’t ‘how to tax crypto’-it’s ‘can the state survive without controlling the narrative of value?’

Rod Petrik

January 17, 2026 AT 09:28Pramod Sharma

January 17, 2026 AT 15:07nathan yeung

January 18, 2026 AT 08:57Man, I get why people are pissed. 30% on gains with no loss offset feels brutal, especially if you’re just trying to recover from a bad trade.

But honestly? I’d rather pay the tax than risk getting dragged into a 10-year audit. I’ve got friends who tried to play smart with P2P and now they’re getting letters from the tax guy. Not worth it.

Also, the GST on wallet fees? Yeah, that’s annoying. But if it means platforms stay legit and don’t vanish overnight, I’ll take it. Better than losing your coins to some shady exchange that disappears with your funds.

Just keep your records. Use a tracker. File on time. It’s not fun, but it’s the least painful way through this mess.

Bharat Kunduri

January 19, 2026 AT 06:22Andre Suico

January 19, 2026 AT 11:58While the regulatory framework appears punitive, its intent may be less about revenue and more about establishing a baseline of accountability in a previously unregulated space.

It is worth noting that the 1% TDS and GST on services create an audit-ready trail, which, while burdensome, also protects compliant users from future claims of unexplained wealth. In jurisdictions with weak financial oversight, such traceability is a shield, not just a sword.

Moreover, the absence of loss offset is indeed harsh, but it prevents complex tax arbitrage schemes that have plagued other markets. Simplicity, even if severe, reduces ambiguity.

The real challenge lies in enforcement equity. The system must be applied uniformly-whether the trader is a retail investor or a high-net-worth entity. Without that, trust erodes.

For now, compliance remains the most prudent path. The alternative is not freedom-it’s vulnerability.

Chidimma Okafor

January 20, 2026 AT 14:27India’s approach to crypto taxation is a masterclass in controlled suppression. The 30% tax, the TDS, the GST on every service-it’s not about revenue, it’s about containment. They know crypto is the future, but they fear losing control over monetary narratives. So they make it so painful to participate domestically that only the most compliant, the most cautious, or the most desperate remain.

Meanwhile, the diaspora thrives in Dubai and Singapore, building real infrastructure while India’s exchanges wither. The irony? The government is creating the very brain drain it claims to want to prevent.

And yet, the system works. It works because it’s designed to intimidate, not to enable. The drop in trading volume isn’t a failure-it’s the goal.

But history shows that suppressed innovation doesn’t disappear. It migrates. And when it returns, it won’t come with permission slips. It’ll come with power.

For now, report your trades. Keep your receipts. But don’t fool yourself: this isn’t taxation. It’s a warning shot.